January 26, 2026 · 8 mins read

Santosh Kumar

Credit cards being accepted on UPI (Unified Payments Interface) have a significant impact on the way users make digital payments in their day-to-day lives. Users typically expect the payment experience of a UPI payment made using a credit card to feel similar to a UPI payment made with a bank account; however, the processing of the transaction is subject to the credit card rules. When a UPI credit card payment is refunded or reversed, the difference will be most relevant to you.

As a UPI credit card user, you may not know what to expect with regard to the timing of your refunds, how your UPI credit card statement will be reflected on your account and how this will affect your credit limit and outstanding balance. If you know how the refund process for a UPI credit card transaction works, you will be better informed and prepared to manage your credit card more effectively.

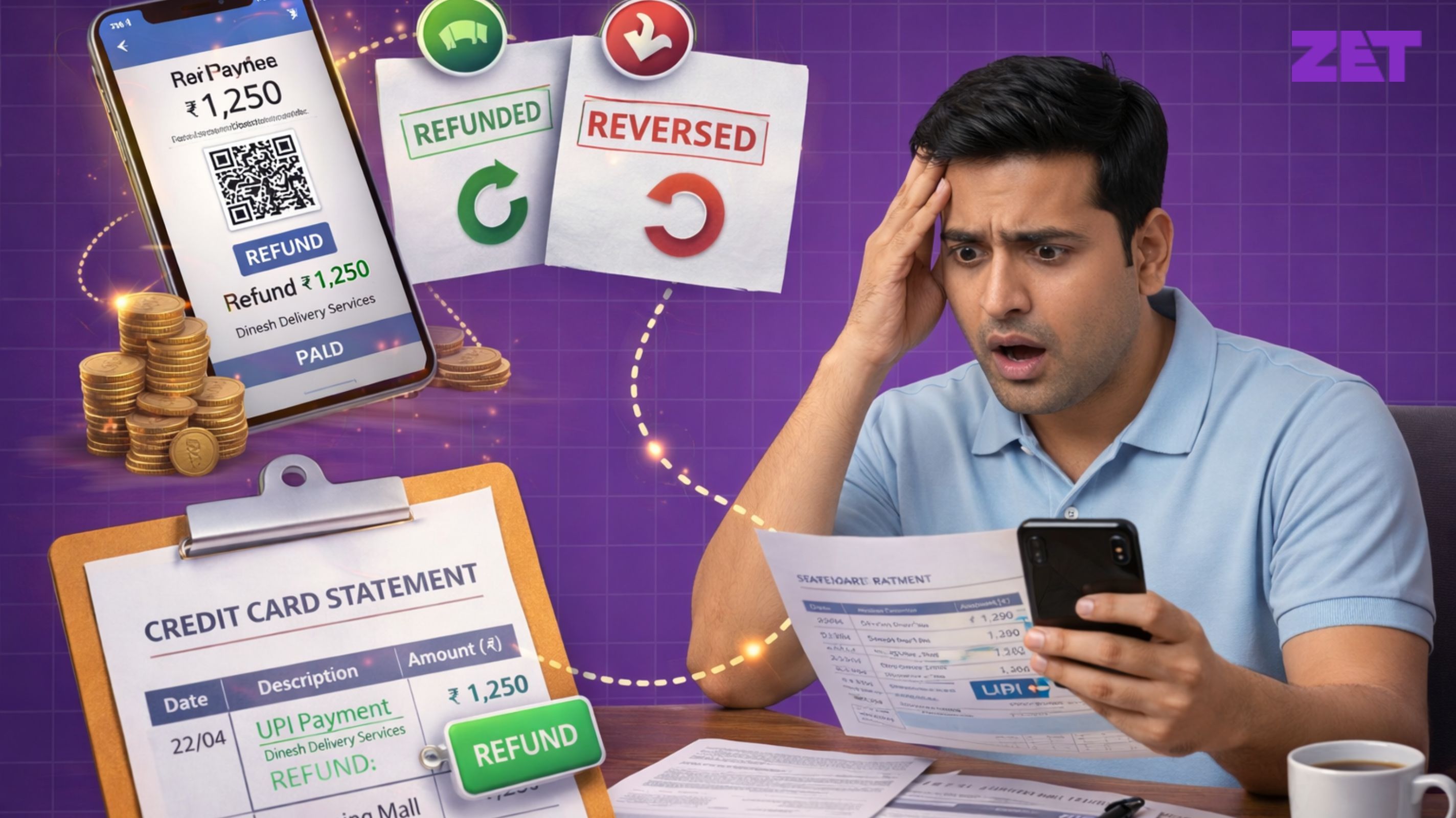

When a UPI credit card transaction is reversed or refunded, it is generally because the merchant has refunded the money to you. This may occur due to a dispute between you and the merchant, or because of a failed settlement. Although you may initiate the request through the UPI app, the processing of the refund is handled through your credit card issuer. Because of this, the timeframe for refunds from UPI credit card transactions will follow the credit card settlement cycle, not the usual instant reversal timeline associated with UPI transactions.

The refund process for a completed UPI credit card payment will take longer compared to the refund process for a completed bank account UPI payment. When a credit card charge is submitted to the credit card network for processing, the credit card network must first verify that the merchant has authorized the charge before making any changes to the credit card account.

Also Read: Can Students Get a ₹2,000 FD Credit Card? A Complete Guide

If a UPI Credit Card payment is refunded, the refund will show as a credit on the credit card statement, which reduces the total outstanding balance on the credit card and restores the available credit limit. Generally, this entry includes information that identifies the original transaction or merchant, making it convenient to identify.

As the original source of funding for the UPI Credit Card payment was a credit card, the refund will only show on the credit card statement for the associated billing cycle. Refunds processed after the release of the associated billing cycle statement will show up on the next billing cycle statement.

Also Read: ₹2,000 FD Credit Card Limit: How Much Limit Can You Get?

Refunded amounts are considered payments towards the outstanding balance. If a refund occurs before the due date for the relevant billing cycle, the refund decreases the amount of the outstanding balance owed. Alternatively, if a refund occurs after the due date for the relevant billing cycle, the refund amount will be applied towards payment amounts owed in future billing cycles.

Refunded amounts that are processed to customers who have already paid the total balance due will create a credit balance on the customer's card account. Customers are able to utilize the credits on the next transaction or keep them as a separate credit until they are used on future transactions.

Also Read: How to Get a Credit Card with Just a ₹2,000 FD in India

Your credit limit will be reinstated to what it was prior to the refund as soon as the refund has cleared. Though this reinstatement of your credit limit will happen relatively immediately with most card issuers, it may not take place right away for some bank/financial institutions, and so a credit card account may appear to have less accessible credit due to refunds already being initiated, but not yet completed through the card network. This temporary disparity in available credit will be eliminated when the entire process associated with your refund has been completed and reflected in the credit card processor's system.

As far as a timeline for processing a UPI credit card refund, it will depend on the merchant used for the purchase, the card network processing that merchant's payment, and the bank or financial institution that issued the card you used. Even if the UPI app indicates that a refund initiation was completed successfully, it does not mean that your credit card account has received the money. Therefore, it may take a few business days for the refund to be reflected on your credit card account statement. This is also considered to be a normal part of the refund process and does not mean that the refund is unsuccessful.

The timeline for processing UPI credit card refunds that were requested due to technical issues will also differ from the timeline for other refunds, but they will be processed according to the standard credit card settlement rules. Therefore, it is recommended that you rely on your credit card statement to confirm if the refund has been successfully credited to your credit card account rather than relying on notifications received from the UPI app.

Also Read: How to solve ‘UPI ID Not Found’ error?

If a payment on a bill made via UPI credit card is refunded to the cardholder but the consumer had already paid either some or all of the bill, the amount refunded will post back to the user's account (credit) with the credit card company and the user's account. The amount that is received may either be applied against any future balances due by the user, creating a decrease in what the user owes or may create a positive balance on the user’s account. Only if the cardholder specifically requests it will the user's balance be returned to their bank account by the card issuer. The credit balance can be tracked through the statements the cardholder receives. In order to properly account for refunds properly, the user should carefully review the statement that covers the billing period immediately following the credit for the refund.

There are no interest charges on refunded purchases as long as the cardholder pays the entire balance within the interest-free grace period. In the case of a late refund, if the cardholder does not pay the total amount owed, there may be temporary interest until the refund appears in the cardholder's account. The refund will be applied to the account's total outstanding balance. If the issuer has already charged a cardholder any fees or other amounts, those charges will not be reversed just because the issuer provides a credit for the transaction in question. Therefore, cardholders should check their statement to verify that the transaction has been properly credited.

Also Read: What Is UPI 123Pay and How to Use It Without Internet?

A UPI Credit Card Refund typically appears in your statement within a few working days after the refund appears in your account. This can differ depending on the merchant and credit card issuer.

No, the UPI Credit Card Refund does not go back into your bank account; it will be credited back to the credit card account of the credit card used to pay for the purchase.

Once the refund is posted in full to your credit card account, it will restore your credit limit, but it is possible that it may not happen immediately.

As long as you are not paying the previous balance in full, you will have to pay interest temporarily until the refund is credited to your credit card.

YES! You can initiate a chargeback or a dispute due to not receiving your refund or receiving it later than expected by contacting your credit card issuer.

Contact

care@zetapp.in

Social

Build and Maintain a 750+ Credit Score